During 2022, expectations for global economic growth have declined as the dark clouds of accelerating inflation, rising interest rates and the Russian invasion of Ukraine gather on the horizon. This also has both direct and indirect effects on global pulp markets.

“Short-term turbulence is possible in the pulp markets,” says John Litvay, partner at the consultancy company Brian McClay & Associates (BMA).

BMA has reduced its estimate for pulp market growth in 2022 and 2023 amid forecasts for declining global economic growth. Consumption growth is expected to be 1.7 per cent annually.

Tomi Amberla, director of AFRY Management Consulting, also sees the short-term outlook as more challenging than before. Inflation, slowing economic growth and the global political situation could reduce the demand for pulp.

“Pulp demand varies from year to year. It is greatly affected by general economic development,” he points out.

We expect the demand for pulp to grow at an average annual rate of 2.5 per cent over the next 10–20 years.

Steady long-term growth

However, experts say that the long-term growth outlook for the pulp market has not changed.

“We expect the demand for pulp to grow at an average annual rate of 2.5 per cent over the next 10–20 years,” says Litvay.

In a study conducted for the Finnish Forest Industries Federation last year, AFRY estimated that the global pulp market will grow by 1–3 per cent annually up to 2035. Amberla says this estimate still holds true.

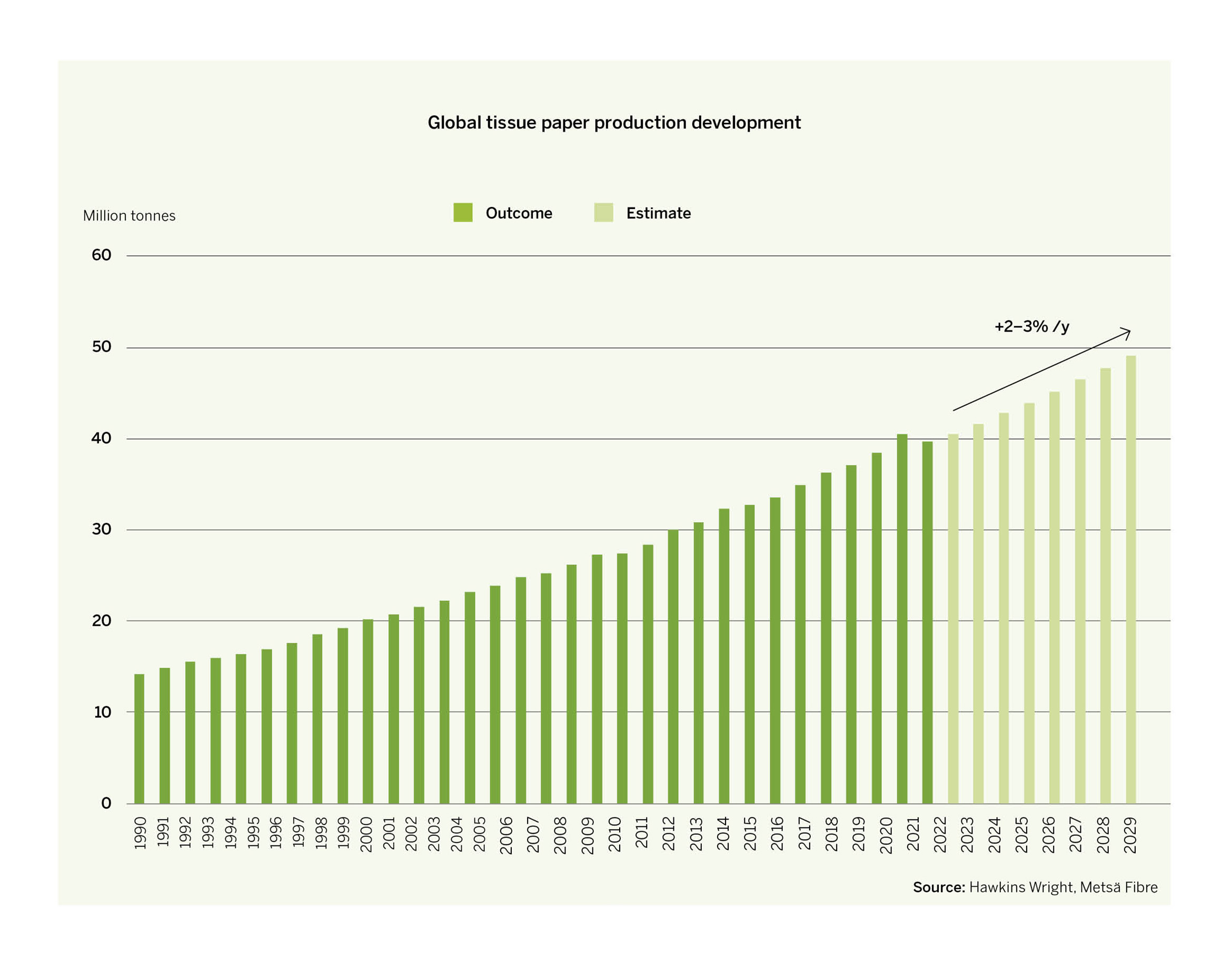

Oliver Lansdell, director of the consultancy company Hawkins Wright, says a key driver of pulp market growth is the increasing consumption of tissue paper, particularly in emerging markets. Most tissue is made from market pulp.

“We expect the demand for tissue paper to grow by 2–3 per cent per year in the long term,” he estimates.

Megatrends underpin growing demand

The growing consumption of tissue paper is fundamentally linked to megatrends such as urbanisation and increasing consumer purchasing power, which continue to gain momentum, particularly in emerging economies.

“Global megatrends are underpinning basic pulp demand growth, as the use of both packaging paperboard and tissue paper products is increasing. These will provide a solid basis for demand growth in the long term. Of course, there will continue to be cyclical fluctuations between years,” says Amberla.

A good example of growing product categories are hygiene products made of tissue, such as toilet paper, and paper hand towels and handkerchiefs.

Meanwhile, the demand for pulp-based paperboard and other packaging materials is growing as living standards in emerging economies improve. Instead of visiting traditional market stalls, more and more consumers are buying packaged food from grocery stores.

The fast-growing online shopping sector also requires more packaging materials to transport products.

The global green transition away from fossil raw materials is driving demand for pulp.

Wood fibre offers alternatives to plastic

The global green transition away from fossil raw materials is driving demand for pulp, says Lansdell. Any alternative materials must be renewable with a low carbon footprint. An example of this is seen in the packaging industry which is looking for solutions to replace plastics in disposable dishes and food packaging.

“Fibre-based alternatives to plastic bottles are also being sought. All these applications require both recycled and fresh fibres. In the coming years, we will certainly see more innovations based on wood fibre,” he says.

This development is being driven by legislation that restricts the manufacture of products made from fossil raw materials. The EU has already banned certain single-use plastic products and many countries have restricted the use of plastic bags, for example.

Litvay points out that cellulose-based textile fibres will also play an increasingly important role in the global textile market in the future.

“The demand for sustainably produced textile fibres will grow as oil-based materials are replaced by less environmentally harmful alternatives. In addition, cotton cultivation is under pressure as it uses a lot of water and takes up space that could be used for food production,” he says.

Lansdell agrees that textiles made from wood fibres will make a breakthrough in the coming years.

“Finland is one of the pioneers in developing new technologies. Though production is still expensive, costs are falling. The opportunities are enormous. Consumers, governments and NGOs alike want new alternatives to polyester and cotton.”

Demand for all pulp grades

Amberla says the long-term growth outlook is bright for all pulp grades.

“Megatrends will have a positive impact on the demand for both bleached and unbleached softwood and hardwood pulp.”

Bleached softwood and hardwood pulp is required for applications such as tissue paper, packaging materials and office paper. The demand for unbleached pulp is driven by packaging, which is required for transporting goods bought online as well as for food packaging.

“The demand for unbleached pulp is increasing due to Chinese import restrictions on recycled paper. In the production of packaging board, fresh fibre is then required to replace it,” Litvay points out.

Growth focus on Asian markets

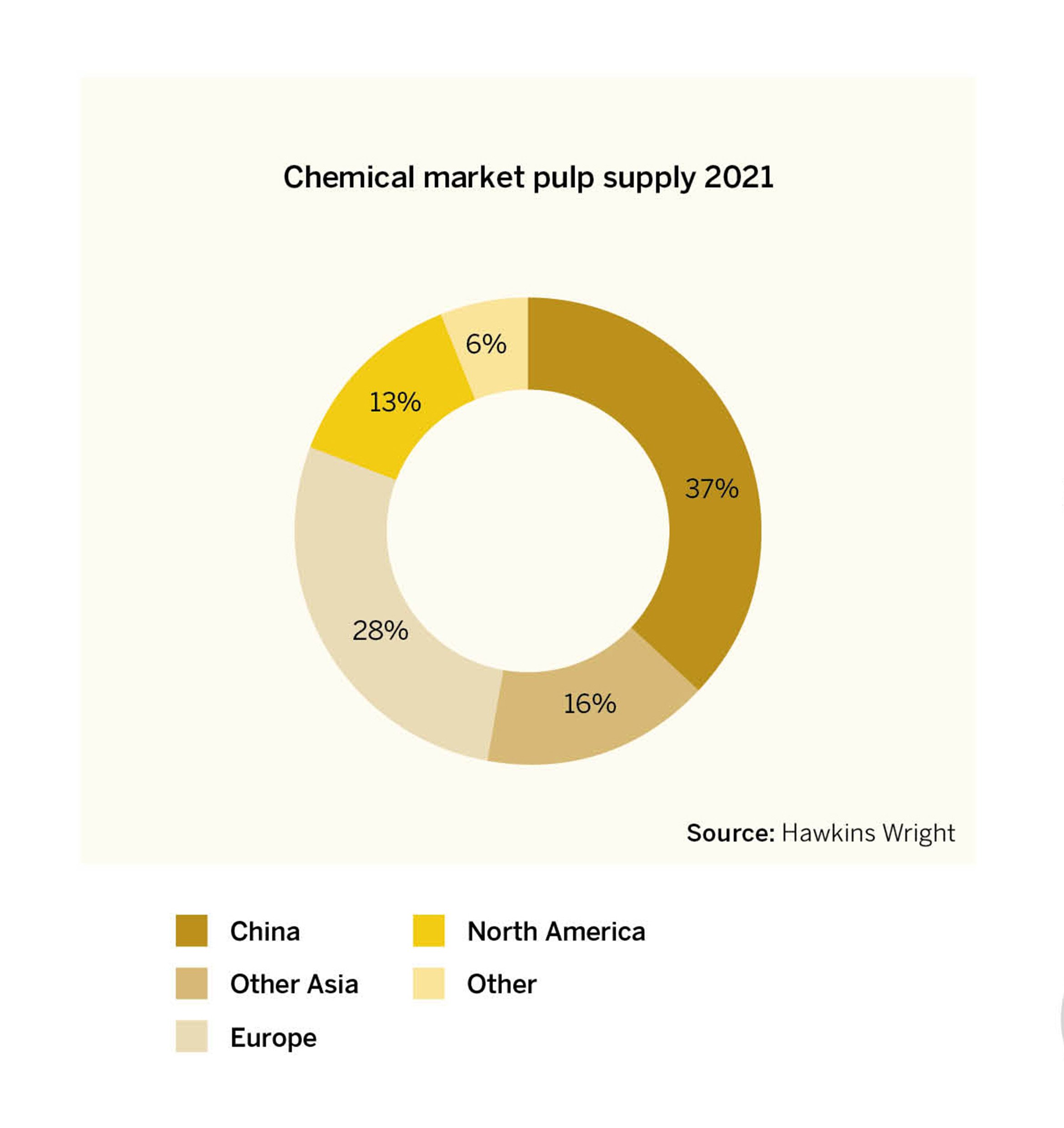

In the future, China will play an increasingly important role in the global pulp market. Its share of market pulp consumption has risen to around 40 per cent.

“China’s already significant paper and board industry will keep growing in the coming years, albeit at a slower pace than before. However, there may not be enough domestically produced fibre available,” says Lansdell.

In addition to China, demand for pulp is growing in other emerging economies. For example, Indonesia, Vietnam, and India are all at different stages of development, but all have a growing and prospering middle class.

The Indian Paper Manufacturers Association (IPMA) expects paper consumption in India to grow by 6–7 per cent in the coming years.

“The availability of wood is poor in regions with the world’s highest population growth. Market pulp is the most economical way to get raw material for local paper mills, as it is not economically feasible to ship products like tissue paper across the seas,” says Amberla.

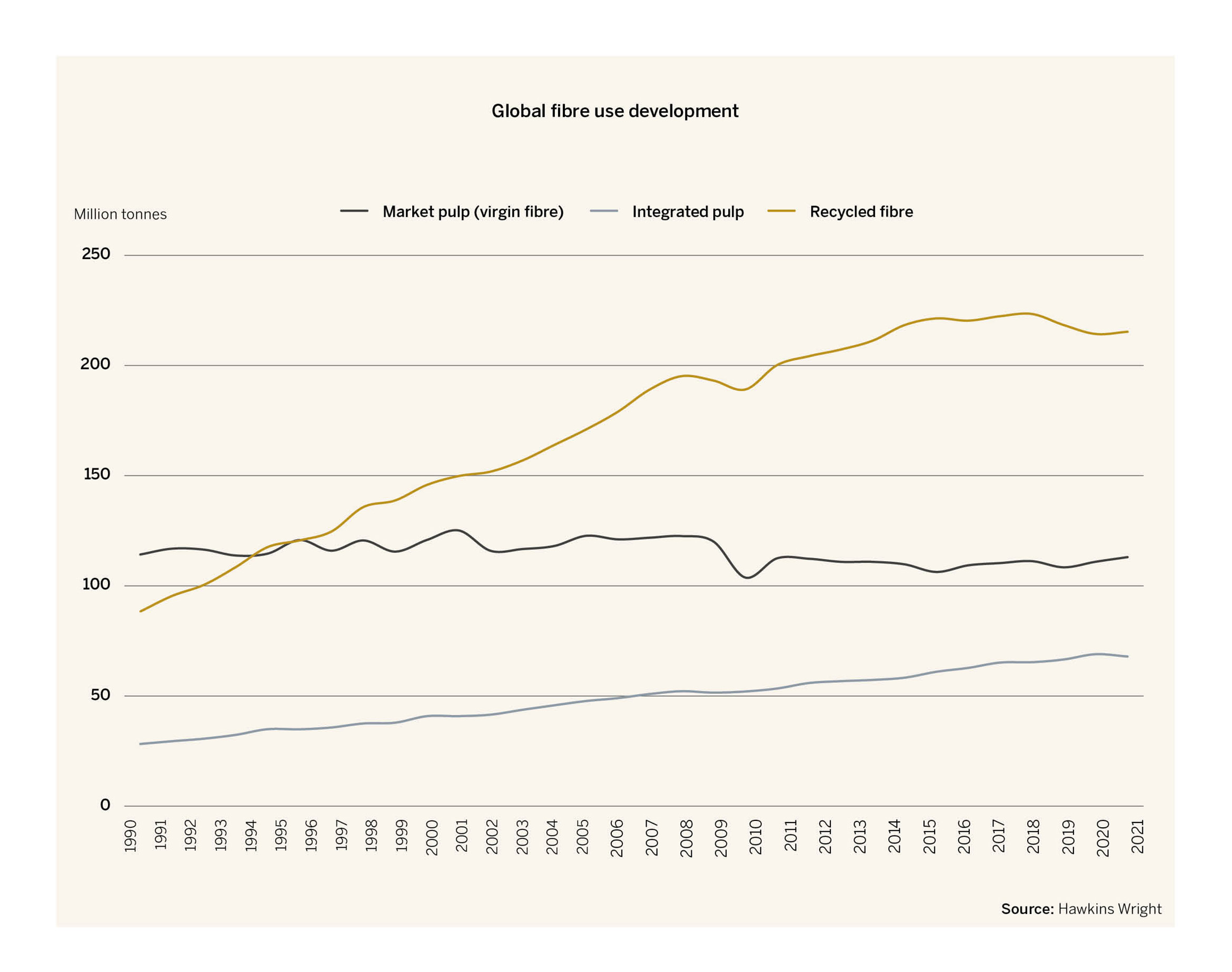

He points out that global demand for pulp is also being boosted by a decline in the amount of high-quality recycled fibre, which is due to a decline in the consumption of printing and writing paper in Europe and North America.

“The recycled paper that is not available has to be replaced by fresh fibre in the manufacture of new products.”

Increasing volatility in pulp markets

Predicting pulp prices has never been easy, but Amberla says it has become even more challenging due to increased volatility, in other words, price fluctuation. This is primarily due to China becoming one of the largest buyers of pulp globally.

“The Chinese pulp market is inherently speculative. Volatility is further increased by the growth of the country’s own pulp production capacity, as there are large fluctuations in the production volumes of local pulp mills.”

When the price of domestically sourced wood raw material and imported wood chips is low, it is worth running mills at full capacity. When raw material is expensive, more market pulp is used for paper production in China.

Volatility in the international pulp market is amplified by changes in pulp supply around the world. Amberla says there have been more supply shocks recently than in the past for various reasons.

The Covid-19 pandemic has disrupted production and supply chains at some mills in North America and other places. Congestion in major ports and occasional container shortages have also affected pulp shipments.

Climate change is also having an impact on pulp markets. For example, exceptional weather conditions have hampered production plant operations in Canada, with floods and landslides caused by heavy rainfall disrupting road and rail links in British Columbia last year.

This article was originally published in Fibre Magazine issue 2022–2023.